How NSW’s $15,000 Interest-Free Solar Loan Works

The NSW Government has introduced the Home Energy Saver Scheme to help homeowners with the upfront cost of electrifying their homes. From 17 June 2026, eligible households can borrow up to $15,000 for solar and other energy upgrades at zero interest, then repay it over as long as ten years. Here is how the NSW $15,000 interest-free solar loan works, who qualifies, and how to apply.

What is the NSW Home Energy Saver loan?

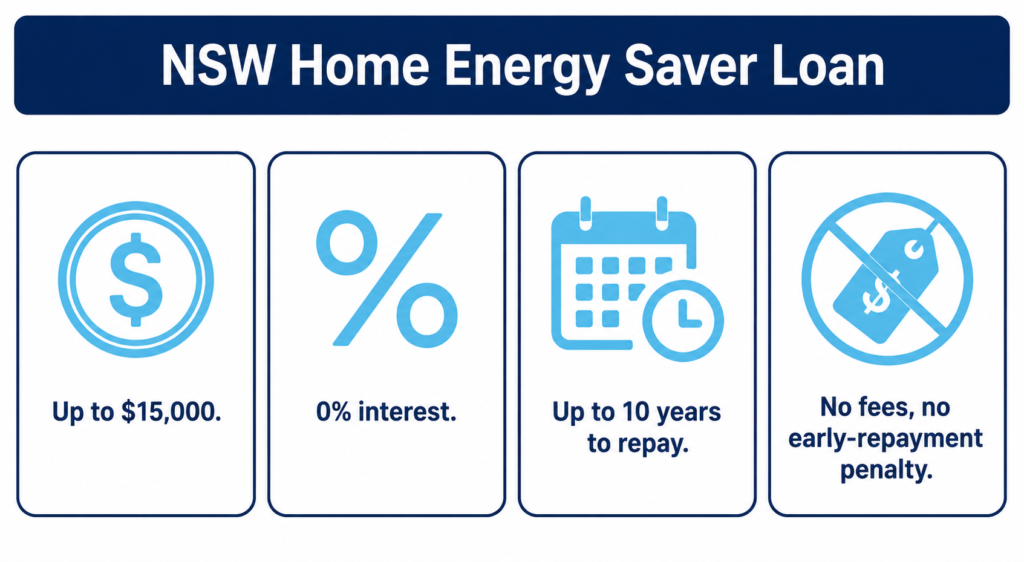

The Home Energy Saver loan is an interest-free loan of up to $15,000 per property, funded by the NSW Government and delivered by two private finance providers, Brighte and Plenti. The key features are:

- Up to $15,000 per property, with no interest charged.

- No fees. No upfront fee, no monthly fee, and no penalty for paying it off early.

- Up to ten years to repay, so you only ever repay what you borrow.

- A loan, not a grant. Applications opened on 17 June 2026, with no closing date set.

One point matters more than people expect: you never handle the money yourself.

- The finance provider pays your accredited installer directly.

- Payment is released only once you and the installer both confirm the work is done.

- You can bundle several upgrades into one loan up to the $15,000 cap.

- If your project costs more, you pay the difference to the installer.

Who is eligible for the NSW solar loan?

To take the loan, you need to tick every box below:

- You own the property, as either an owner-occupier or a landlord.

- Your combined annual taxable household income is below $210,000.

- You are an Australian citizen or permanent resident.

- You pass the finance provider’s credit check.

- The property is in NSW.

- The property is not social housing or used for short-stay accommodation.

A couple of situations to note:

- Renters cannot take the loan, though they may access a separate discount with their landlord’s permission.

- Strata or apartment dwellers can apply, but you must get owners-corporation approval for the upgrade yourself.

What can you spend the loan on?

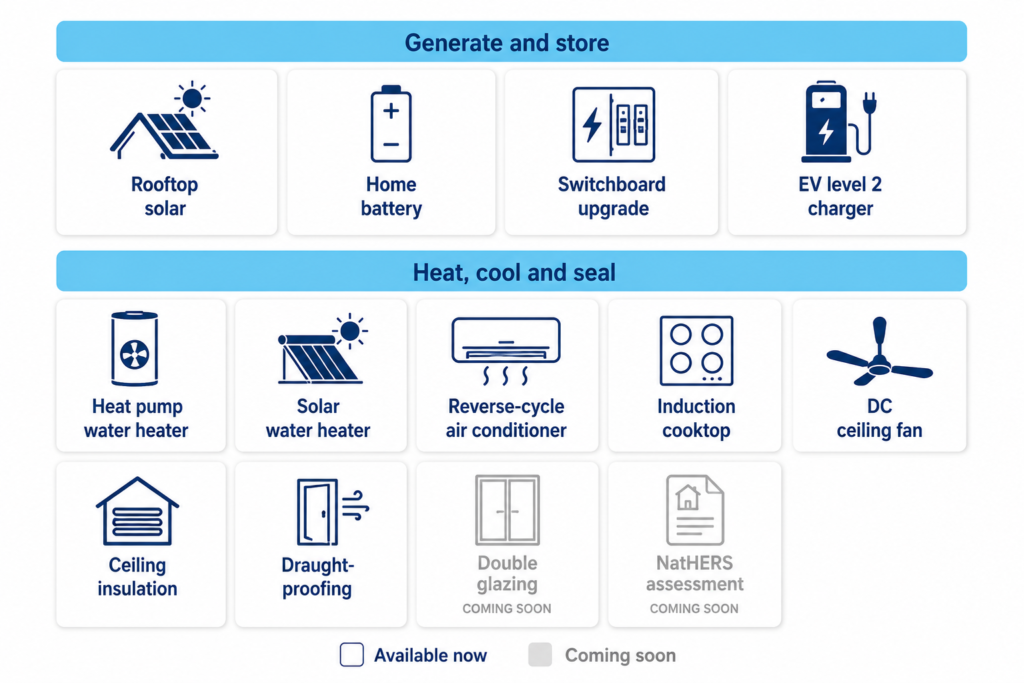

The scheme covers thirteen upgrade types:

- Rooftop solar

- A home battery

- A switchboard upgrade

- A heat pump water heater

- A solar water heater

- A reverse-cycle air conditioner

- An induction cooktop

- An EV level 2 charger

- A DC ceiling fan

- Ceiling insulation

- Draught-proofing

- Double glazing

- A NatHERS home energy assessment

Each lender currently funds a narrower part of this list while more categories are added, so check what your provider offers before you commit. If solar is your first step, it helps to work out what size solar system you actually need before you ask for quotes.

One detail worth knowing: any federal or NSW incentives you qualify for are applied before the loan amount is worked out, which can reduce how much you need to borrow.

How do you apply for the NSW Home Energy Saver loan?

The process runs in a clear order:

- Check your eligibility using the loan guidelines or the NSW Energy Savings Finder.

- Choose your upgrade. The NSW Energy Savings Calculator can help you compare savings.

- Pick a finance provider, either Brighte or Plenti.

- Get quotes from approved suppliers.

- Finalise your application on the provider’s website.

The step most people miss is that you can only apply through a program-approved, accredited vendor. The vendor refers you to the finance provider, who then sends you a unique link to finish the application. Often the easiest route would be to reach out first to a trusted local installer and take advantage of their experience to enter into the scheme.

If you are weighing up incentives, it is worth understanding how the federal and NSW battery rebates stack alongside this scheme.

Is the solar loan worth using?

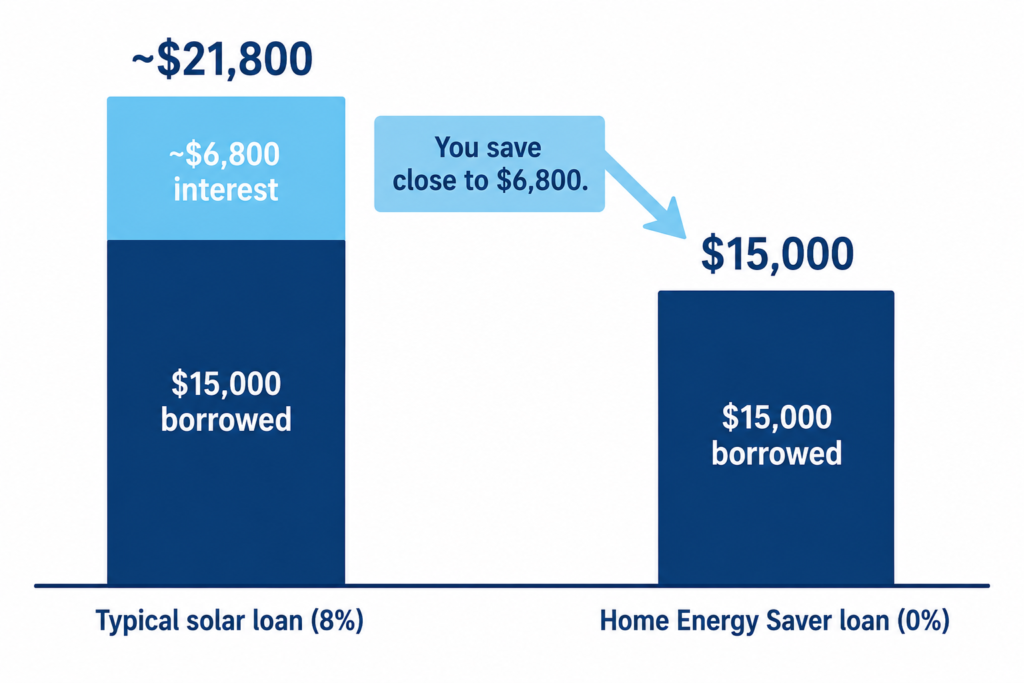

Most loans for a solar and battery system currently start at around 8% interest. On a $15,000 loan repaid over ten years, that adds up fast. At 8%, you would pay roughly $182 a month and hand over close to $6,800 in interest on top of the $15,000 you borrowed. Under the Home Energy Saver loan you pay none of that. The $15,000 is all you ever repay, so the saving is close to $6,800 compared with a typical loan.

A solar and battery system is still the most effective way to bring down your electricity bills, and with the rebates available right now the value on offer to homeowners is excellent. Between the interest-free loan and existing federal and state incentives, there has rarely been a better time to consider a system. The smartest order is simple:

- Speak with a specialist in the field.

- Settle on your upgrades.

- Apply through an accredited Brighte or Plenti vendor.

Considering a battery? Read our article on the Mistakes to Avoid When Buying a Solar Battery

Frequently Asked Questions

Who is eligible for the NSW $15,000 interest-free solar loan?

You need to own the property as an owner-occupier or landlord, have a combined annual taxable household income of up to $210,000, be an Australian citizen or permanent resident, and pass the finance provider’s credit check. The property must be in NSW and cannot be social or community housing or used for short-stay accommodation. Renters are not eligible for the loan, but they can access the separate $4,000 discount with their landlord’s permission.

How do I apply for the NSW Home Energy Saver loan?

Start by checking your eligibility through the loan guidelines or the NSW Energy Savings Finder, then choose your upgrade and a finance provider, Brighte or Plenti. You apply through a program-approved, accredited vendor, who refers you to the provider. The provider then sends you a unique link to complete the application. The loan money goes straight to your installer once the work is confirmed, so you never receive cash yourself.

Can I use the Home Energy Saver loan for both solar panels and a battery?

Yes. You can bundle several eligible upgrades, including rooftop solar and a home battery, into a single loan up to the $15,000 cap. If the combined cost is higher than $15,000, you pay the difference to your installer. For help sizing a system to your home and budget, see how to choose a solar battery size.